Microfinance clients are a heterogeneous group, and their characteristics vary significantly from one region to another. The characteristics of microfinance clients have altered recently, according to a growing body of research. This evidence suggests that the clientele of microfinance institutions (MFIs) has changed significantly over time.

The changes in the clientele of MFIs can be attributed to several factors, including the expansion of microfinance services to new geographic areas and client segments, the entry of new players into the market, and the industry’s increasing maturity.

The evidence of the changes in the characteristics of microfinance clients is primarily based on surveys of MFIs. Several organizations have conducted these surveys, including the Microcredit Summit Campaign, the Consultative Group to Assist the Poor (CGAP), and the International Fund for Agricultural Development (IFAD).

The findings of these surveys indicate that the clientele of MFIs has become more diverse over time. In particular, the share of women clients has increased, the share of rural clients has declined, and the share of clients from low-income households has remained relatively stable.

The evidence of the changes in the characteristics of microfinance clients has important implications for the design and delivery of microfinance services. In particular, it suggests that MFIs need to be more flexible in their approach to serving clients and that they need to tailor their services to the needs of the changing clientele.

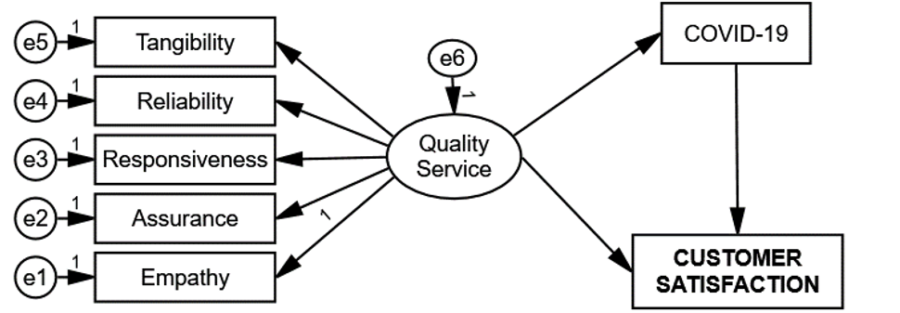

Satisfaction of Microfinance Clients

Microfinance clients always seek better services and products to make their lives easier. They are also always looking for changes that will improve their financial well-being. This is why microfinance institutions must proactively offer new and improved services to their clients.

Many factors can affect the satisfaction of microfinance clients. Some of these include the quality of service, the availability of products, the transparency of pricing, and the responsiveness of customer service.

The overall reputation of the microfinance institution also influences microfinance clients. If an institution has a good reputation, attracting and retaining clients will be easier. On the other hand, if an institution has a bad reputation, it will be harder to attract and retain clients.

It is essential for microfinance institutions always to keep their clients satisfied. This can be done by constantly innovating and improving their products and services. It is also essential to be responsive to clients’ needs and always offer transparent pricing.

The Impact of Changes on Microfinance Clients

Microfinance clients are often susceptible to changes in the products and services they receive. This is because they often have minimal options when it comes to financial services, and any change can have a significant impact on their lives.

For microfinance institutions (MFIs), this means that any changes to their products or services need to be carefully considered and implemented in a way that minimizes the impact on clients. MFIs also need to be prepared to deal with any negative feedback from clients who are unhappy with changes.

In some cases, changes to microfinance products and services can positively impact clients. For example, if an MFI introduces a new product that meets the needs of its clients better than its existing products, this can lead to increased client satisfaction.

However, changes can lead to client dissatisfaction, primarily if not implemented properly. For example, if an MFI introduces a new fee without adequately explaining it to clients, this can lead to confusion and frustration.

MFIS need to consider the potential impact of changes on their clients when making decisions about changes to their products and services. Careful planning and communication can minimize changes’ negative impact and ensure that clients remain satisfied with the microfinance products and services they receive.

The Future of Microfinance

Microfinance has come a long way since its inception in the 1970s. What started as a way to provide small loans to the poor has grown into a multi-billion dollar industry. Over 1,000 microfinance institutions (MFIs) worldwide, reaching over 150 million clients.

Despite its growth, the microfinance industry is still facing many challenges. One of the biggest is the high-interest rates charged by MFIs. In some cases, these rates can be as high as 60%. This makes it difficult for clients to repay their loans and can trap them in a cycle of debt.

The absence of transparency in the sector is another problem. Many MFIs are not required to disclose their financial statements or loan terms. This makes it difficult for clients to decide about taking out a loan.

These challenges will likely shape the future of microfinance. MFIs must find ways to reduce their interest rates and increase transparency. They will also need to expand their reach to new markets.

One way MFIs can reduce their interest rates is by increasing their efficiency. Many MFIs still rely on paper-based systems, which can be costly and time-consuming. Switching to digital systems can help MFIs save money and pass the savings on to their clients.

Another way to reduce interest rates is by increasing competition in the industry. This can be done by encouraging new entrants and supporting the growth of existing MFIs.

Finally, MFIs need to expand their reach to new markets. This includes serving clients in rural areas and providing loans for new purposes, such as education or housing.

The future of microfinance is full of challenges but also opportunities. MFIs that can adapt to the changing landscape will be well-positioned to succeed.

1 Comment

https://prestigeautodetailingkc.com

Thanks-a-mundo for the article post. Fantastic.